Get Instant Solution By an Expert Advisor

(4.8)

Fast replies · No spam · Real experts

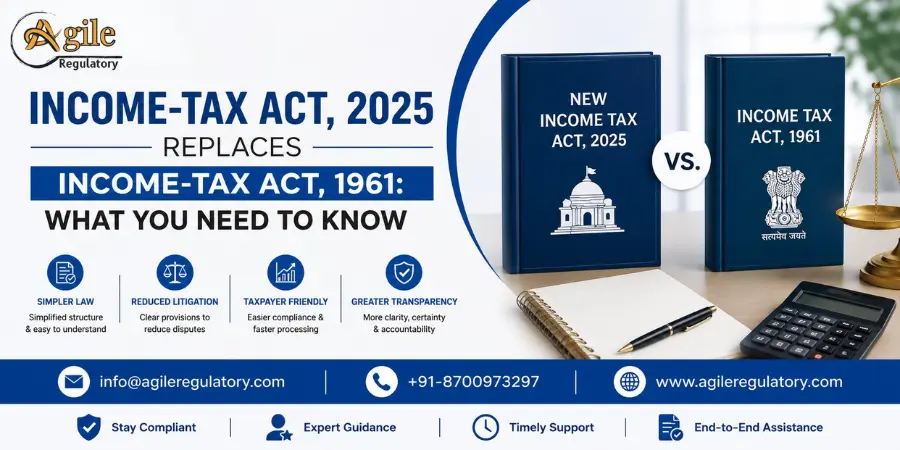

India’s tax law has just received its first real overhaul in more than 60 years and for most taxpayers the changes are less dramatic than they sound.

The Income-tax Act, 2025 shall replace the 1961 Act from 1 April 2026. But the thing is the tax rates, deductions and exemptions haven’t moved. What has changed is the structure, the way the law is written, organised and read.

For years the old Act was patched and mended. By the end it was a maze of provisos, cross-references and explanatory clauses that even experienced CAs found maddening. The 2025 Act cuts more than 800 sections to 536 in 23 cleaner chapters.

A note of clarification: The 1961 Act continues to apply for FY 2025-26 and prior years. The new law would come into effect from FY 2026-27.

Gone are the terms "Previous Year" and "Assessment Year." The new Act introduces a single concept the Tax Year. So Tax Year 2026-27 simply means April 2026 to March 2027.

Under the 1961 Act, registration, exemptions, and donor deduction rules were scattered across multiple sections. The 2025 Act pulls them together under Chapter XVII-B (Sections 332 to 355)

All qualifying organisations previously registered under Sections 12A, 12AA, 12AB, or 10(23C) will now be called Registered Non-Profit Organisations (RNPOs). The transition is automatic. If your registration was valid as of 31 March 2026, you carry forward as an RNPO without reapplying. The original expiry dates hold.

New registrations fall under Section 332 which consolidates what was previously split across three different sections.

The paperwork has been renumbered:

Form 104 replaces Form 10A (provisional registration)

Form 105 replaces Form 10AB (regular registration and renewals)

Smaller organisations get meaningful relief here. Trusts with annual income under ₹5 crore in each of the two preceding Tax Years now qualify for a 10-year registration double the five years permitted earlier.

Donor deduction approvals move to 80G Section 354 Registration. Existing approvals stay valid till their current expiry, and renewals go through Form 105.

One thing to keep track of: RNPO registration and Section 354 approval run on separate clocks.

RNPO registration can last up to 10 years

Section 354 (donor deduction) approval still needs renewal every five years

Applications for renewal should ideally be submitted at least six months before expiry. Organisations whose registrations had already lapsed before 1 April 2026 will need to apply fresh under Section 332.

Quite a lot, actually.

The 85% application rule remains intact RNPOs must still direct at least 85% of their income toward charitable or religious purposes to claim full exemption. Judicial precedents built around charitable exemptions over the years are expected to stay relevant.

The one procedural relaxation: the deemed application option can now be exercised up to the ITR filing due date, instead of two months ahead of it. Small change, but a useful one for organisations that cut it close.

The Income-tax Act 2025 is a re-writing not a re-invention. The day-to-day compliance for most trusts and NGOs looks the same under a tidier framework. The real ask is to stay on top of the new section numbers updated forms and the separate renewal timelines for registration vs donor approvals.

Proven 4-step Process: Consultation, Documentation, Submission, and Certification

What our customer says about us

Lavkush Sharma

KTPL Instruments

Agile Regulatory handled my BIS Certification registration smoothly. Their expert team ensured quick approvals, transparent pricing, and a completely stress-free compliance experience.

Nitin Mukesh

Justrack IOT

We are grateful to Agile Regulatory for their excellent support. Their team showed patience, expertise, and professionalism throughout, providing clear guidance and making the entire process smooth and hassle-free.

Pradeep Varma

Coaire Compressor

Being an excellent BIS Certification Consultant provider, they help customers with all requirements such as BIS Certification, CDSCO services, Agile Regulatory support, legal issues, and lab testing with quick results.

Bharat Bachwani

Easy Polymer

With the help of Agile Regulatory, we have made significant progress in our business. Their service is fast, genuine, and reliable. We look forward to continued success together in the future.

Atul Jain

Tarus International

Many thanks to Agile Regulatory for all the support, guidance, and expert advice. Their professional approach and consistent assistance have made a significant difference.

Paramjeet Singh

Anchor Weighing

Top-tier consulting! offered strategic solutions that revolutionized our approach. Their deep expertise and personalized guidance made a significant impact on our success. Highly recommend their services.

Anshul Rathi

AM Capacitor

Agile Regulatory exceeded expectations! Their tailored solutions, expertise, and proactive approach led to remarkable results. Highly recommend for businesses seeking impactful and strategic guidance.

Shekhar Maurya

Imaxx Pro Aquistic

Outstanding service! delivered targeted solutions with professionalism and expertise. Their insights elevated our business strategies, resulting in noticeable growth. Highly recommended for exceptional consultation.

Trusted by over 1,00,000 + Global Brands in the past 12 years

Leave a Reply

Your email address will not be published. Required fields are marked *